April Insights: Markets, Policy, and a little Fun

Spring is here — and with it, fresh market perspectives. We start with a technical look at the current drawdown and what it means for long-term strategies. Next, we cover A Family Guide to Trump Accounts (otherwise known as Section 530A Accounts). Don’t miss our Ask Sabrina meeting on ClientWorks and WealthVision, plus Brock’s fun image to brighten your inbox.

A little April cheer — and plenty of financial clarity.

As the first quarter comes to a close, it’s clear that equity markets have endured a difficult stretch. The strong momentum that drove a record‑setting rally early in the year faded quickly as concerns over artificial intelligence (AI) spending and disruption dampened risk appetite. The outbreak of the Iran war in late February added new challenges, as the essential closure of the Strait of Hormuz underpinned an unprecedented supply shock in oil that quickly drove prices to multi-year highs. Inflation fears promptly followed, and the market drastically repriced global monetary policy expectations to a higher-for-longer regime, with growing probabilities for tightening among major central banks (including the Federal Reserve).

With markets now hinging on when the U.S.‑Iran conflict might be resolved and when the Strait will fully reopen, uncertainty remains the dominant force. The longer the conflict persists, the greater the potential strain on global growth, inflation, interest rates, earnings, profit margins, and ultimately equity markets.

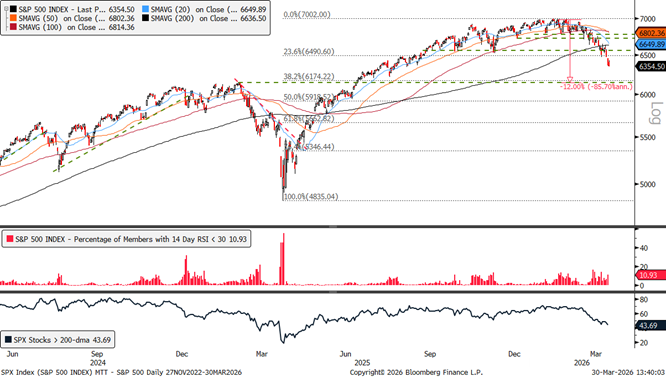

Stocks have struggled against this challenging backdrop. The S&P 500 posted its fifth straight weekly decline last week and is now inching toward correction territory, technically defined by a drawdown of 10–20%. Technical damage has been significant as the index broke below its closely watched 200-day moving average (dma) and the November lows at 6,522. This leaves 6,174 (a key Fibonacci retracement level of the April–January advance) and the February highs at 6,144 as the next major downside support levels to watch.

The consistent pattern of lower highs and lower lows over the past two months has turned near-term momentum gauges bearish. Although oversold conditions are starting to emerge, most indicators have yet to reach the extreme levels that typically signal contrarian buying opportunities. For instance, only about 11% of S&P 500 stocks registered oversold Relative Strength Index (RSI) readings on Friday, well below the +50% seen last April or the +20% levels observed during previous market corrections in recent years.

Selling pressure has also been widespread, and market internals continue to deteriorate. Only 43% of S&P 500 constituents remain above support from their November lows, with a similar share still holding above their 200-dma. Breadth composition is also concerning, as defensive sectors have taken leadership. Technology, the market’s largest weight, has rolled over, while financials and consumer discretionary sit among the weakest areas in our technical work. A durable recovery will require renewed risk appetite across these sectors, along with meaningful technical improvements.

Technical Deterioration Points to Near-Term Downside Risk

Source: LPL Research, Bloomberg 03/30/26

Disclosures: Indexes are unmanaged and cannot be invested in directly. Past performance is no guarantee of future results.

Historical Perspective

Taking a step back to a longer‑term (and more encouraging) perspective, the secular uptrend supporting this bull market remains firmly in place. History also offers reassurance when it comes to geopolitical shocks. As we noted in our March 9 Weekly Market Commentary (Markets Tested as Iran Conflict Continues), “The stock market has demonstrated remarkable resilience in the face of major geopolitical shocks in the past.” Our analysis of more than 80 years of market reactions to 26 distinct geopolitical events shows that the S&P 500 has historically gained an average of 7.8% in the 12 months following such events and finished higher 68% of the time, although past performance does not guarantee future results.

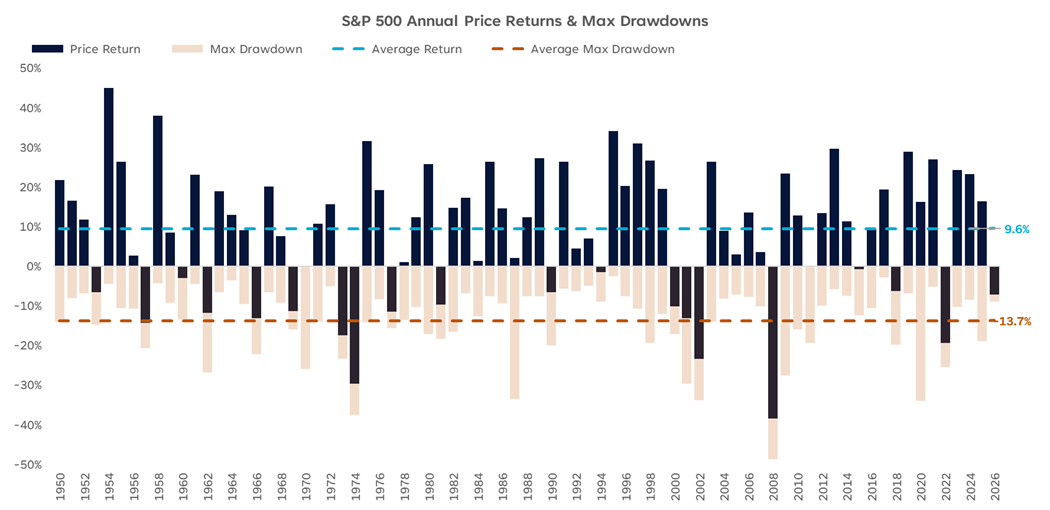

Although drawdowns can feel uncomfortable, particularly following the low‑volatility environment that characterized the start of the year, they should not catch investors off guard. Over the past 75 years, the S&P 500’s average peak‑to‑trough intra‑year pullback has been ‑13.7%. More importantly, despite these declines, the index has delivered an average annual price gain of 9.6%, with positive returns in 74% of those years. As illustrated in the “Bull Markets Are Not Linear” chart, even sizable drawdowns have not necessarily translated to down years. Last year serves as a clear example: equity markets fell nearly 20% in April amid tariff‑related concerns, but as those fears eased and trade policy softened, investor focus shifted back to fundamentals like earnings and economic growth, which helped drive a strong recovery.

Bull Markets Are Not Linear

Source: LPL Research, Bloomberg 03/30/26

Disclosures: Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly. The modern design of the S&P 500 stock index was first launched in 1957. Performance back to 1950 incorporates the performance of the predecessor index, the S&P.

Frequency of Drawdowns

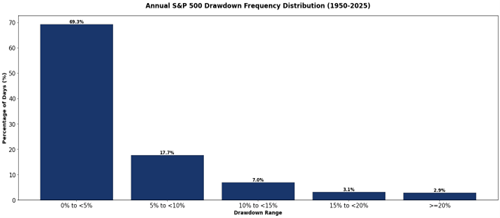

A bull market can sometimes cause investors to forget that drawdowns are not anomalies, they are a normal and frequent part of market behavior. Outside of periods when stocks are setting new record highs, the market is almost always experiencing some degree of pullback. Historically, on a calendar‑year basis, the S&P 500 has spent nearly 70% of trading days in a drawdown of up to 5% and roughly 18% of trading days in a 5–10% drawdown range. Investors may find it reassuring that deeper declines are far less common, as illustrated in the “Drawdowns Should Be Expected” chart.

Drawdowns Should Be Expected

Source: LPL Research, Bloomberg 03/30/26

Disclosures: Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly.The modern design of the S&P 500 stock index was first launched in 1957. Performance back to 1950 incorporates the performance of the predecessor index, the S&P.

Conclusion

Equity markets continue to grapple with mounting near‑term pressures and technical conditions have undeniably weakened. The recent supply‑driven spike in oil prices, rising inflation concerns, and geopolitical uncertainty have all contributed to growing downside risk over the weeks ahead. These forces may keep volatility elevated and leave markets vulnerable to additional corrective price action in the short run.

However, it’s equally important to recognize that the longer‑term backdrop has not fundamentally changed. The secular uptrend supporting this bull market is still intact, and history demonstrates that periodic drawdowns are a routine feature of equity markets rather than a clear signal of imminent long-term destruction. As highlighted earlier, the S&P 500 has spent the vast majority of its trading history in some degree of drawdown, with sizable peak‑to‑trough declines occurring even in years that ultimately delivered strong positive returns. This perspective reinforces the idea that short‑term weakness can coexist with resilient long‑term trends. Please note that past performance does not guarantee future results.

In our view, as long as fundamentals remain reasonably solid and the technical foundation of the longer‑term trend holds, periods of market stress should be viewed through a measured lens. Near‑term downside risks have increased, but the longer‑term technical and fundamental backdrop provide an encouraging counterbalance, in our view.

Did You Know?

A Family Guide to Trump Accounts

(Otherwise known as Section 530A Accounts but officially referred to as "Trump Accounts" on irs.gov)

What You Need to Know

Trump accounts are a new tax‑advantaged way to help children build long‑term savings. They were created under the One Big Beautiful Bill Act (OBBBA), and the IRS outlines the rules in Notice 2025‑68.

What does 530A Mean?

“530A” is simply the Internal Revenue Code section that establishes and governs this account type—similar to how 529 plans and 401(k)s are named after their code sections.

What is a Trump Account?

A Trump Account is a special version of a traditional IRA for children under age 18. It is designed to help families start long‑term savings early, with tax‑deferred investment growth.

Before age 18, the account follows special rules. After age 18, it becomes a standard traditional IRA.

Who Can Open One?

A child qualifies if they:

Are under age 18, and

Have a valid Social Security number.

Only one account per child is allowed.

A parent, legal guardian, adult sibling, or grandparent may file the election to open the account.

Who Manages these Accounts?

According to IRS guidance, management happens in two steps:

Initial Setup: The account must first be opened with a Treasury‑selected trustee to ensure consistent setup and reporting.

After Setup:Families may transfer the account to any eligible IRA custodian, such as a bank or brokerage, through a trustee‑to‑trustee transfer.

Government Contribution: $1,000 for Eligible Children

Eligible children may receive a one‑time $1,000 government contribution if:

They are born on or after December 31, 2024, and before January 1, 2029, and

A U.S. Citizen, and for whom no prior program election has been made

The family files the IRS election form (Form 4547)

No contributions—government or private—can be made until July 4, 2026.

Contribution Rules

Before age 18:

Families may contribute up to $5,000 per year

Employers may add up to $2,500, counting toward the same limit

Contributions are not tax‑deductible, but growth is tax‑deferred.

Investment Rules

Until age 18, investments must be:

Broad U.S. equity index funds

Low‑cost (fees ≤0.1%)

No leverage

These rules keep the account simple and growth‑focused.

Withdrawals

Before age 18: Withdrawals are not allowed, except in rare IRS‑approved situations.

After age 18: The account becomes a traditional IRA, with normal IRA rules for contributions and withdrawals.

Why This Matters

Trump Accounts offer:

Early, long‑term savings for children

A potential $1,000 government boost for eligible children

Tax‑deferred investment growth

A smooth transition into an adult IRA at age 18.

For families focused on long‑term financial planning, these accounts can be a powerful tool.

For Additional Resources, click on the following links:

Need help using Account View or WealthVision? Ask Sabrina is our Q&A session focused on navigating your accounts, accessing statements, and making the most of your tools.

In this session, we will cover Account View and WealthVision 101—navigation, access, and outside account aggregation.

We work for our clients and with them, providing support every step of the way.

Join us Thursday, April 16, 2026, from 1:30–2:00 PM by clicking on link below.

We encourage you to submit your questions in advance to Clients@PlumTreeFinancial.com. This is an open forum, so no client-specific questions, please.

Sabrina, Vice President of Client Services, looks forward to seeing you and answering your questions!

We are back with another look at the Plums' plans, ambitions, and off‑the‑wall musings for 2026. This month, the spotlight shines on Brock. His blend of insight, humor, and inspiration is something you won’t want to miss. Be sure to swing by next month to see which Plum steps up to the stage next.

Upcoming Events

Save the Date

April 21, 2026 | 12pm EST

Market Intelligence – Presented by John Hancock

In today’s global financial markets and nonstop news cycle, it can be hard to cut through the noise and identify the trends that matter most.

Join us for a comprehensive review of the investment landscape across key markets and asset classes that leverages the insight of dozens of asset managers and investment research firms.

Young Investors Series: Invest Now! Or Pay Later...

Join Greg Bernhard and Brock Mumford (members of PlumTree Financial’s investment team) for an engaging session designed specifically for young investors ready to take control of their financial journey.

This webinar will guide you through the essentials of creating a financial plan, including setting meaningful goals, building a budget, starting to invest, and planning for retirement.

Plant the seeds for stronger finances this Spring. Follow us.

Smoke and mirrors - The phrase originates from early-stage magic, where performers used actual smoke and strategically placed mirrors to create illusions that disguised how tricks were performed. The explanation is tied to these visual deceptions, which made ordinary actions appear extraordinary or concealed reality altogether. The old, vivid idiom meaning something intended to mislead or create a false impression—or, in financial/business use, a situation where appearances mask a lack of real value or substance.

Disclosures

Assessing the Impact of Developments in Iran: Watch Energy

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage-backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1086293

Your Family's Guide to Trump Accounts (also referred to as Section 530A Accounts)

Trump Accounts offer tax deferred growth on earnings and provide tax free withdrawals when distributions are qualified.

Contributions may include after tax family contributions, pre tax employer contributions, and a one time $1,000 federal contribution for eligible children born between 2025 and 2028.

Withdrawals prior to age 59½ may result in a 10% IRS penalty tax, in addition to current income tax, and may be restricted until the child reaches age 18.

Annual contribution limits and other restrictions apply.

Some Trump Account rules and regulations are still forthcoming from the U.S. Treasury and IRS.

Clients should consult with a qualified tax advisor or financial professional before making any decisions.

Securities and Advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC. Insurance products offered through LPL Financial or its licensed affiliates.

All information is believed to be from reliable sources; however, PlumTree Financial makes no representation as to its completeness or accuracy.