This month, explore the One Big Beautiful Bill Act — learn what it includes, why it is important, and how it may affect your financial planning. Then, look ahead by Going Paperless, simplifying the way you receive statements, tax forms, and supplemental documents. We are also providing a Mid-Year 2025 Financial Checklist to help you reset and refocus your goals. Finally, enjoy a feature on the refined and lesser-known sport of Court Tennis.

August offers a vibrant combination of structure, strategy, and a touch of the unexpected.

August 2025

Capital Markets

One Big Beautiful Bill Act - Six Takeaways

Adam Turnquist | Chief Technical Strategist, LPL Financial

Last Updated: July 9, 2025

In classic Washington style, Congress pushed the limits of drama and delay, passing a sweeping reconciliation bill just hours before President Donald Trump’s self-imposed July 4, 2025 deadline. After intense negotiations, squabbles within the Republican Party, and nearly an all-night House session, the “One Big Beautiful Bill Act (OBBBA)” squeaked through with a 218–214 vote on July 3, following the Senate’s narrow 51–50 passage, with Vice President JD Vance casting the tiebreaker. Trump signed the legislation into law during a celebratory White House ceremony on July 4, marking a major victory for his second-term agenda.

While there is a lot to unpack within the 869-page text, here are six key takeaways from the bill.

Increased Spending and Work Requirements

As the saying goes, beauty is in the eye of the beholder, so we’ll leave the debate over how “beautiful” the bill is to the media, politicians, and the public. However, most would agree it checked the box for “big.” According to the nonpartisan Congressional Budget Office (CBO), the bill includes $4.5 trillion in tax cuts over the next decade. Given the White House’s focus on national security, the bill boosted defense and border enforcement spending by a total of $300 billion, with $25 billion of that amount earmarked for the “Golden Dome” missile defense system.

To help offset the costs, the bill included $1.2 trillion in cuts to Medicaid and the Supplemental Nutrition Assistance Program (SNAP). New work requirements were also introduced to qualify for assistance. For Medicaid, “able-bodied” individuals without children aged 19 to 64 are required to work at least 80 hours a month to be eligible for assistance (participation in community service, education, or work programs also qualifies). The bill introduced similar, stricter work requirements for SNAP eligibility and mandates that states share at least 5% of the benefit costs starting in 2028.

Overall, the CBO estimates the entire OBBBA will add around $3.3 trillion to the deficit over the next decade.

2017 Tax Provisions Made Permanent

Many of the individual and estate tax provisions from the 2017 Tax Cuts and Jobs Act (TCJA) have been made permanent. This ensures that the current seven tax brackets will remain unchanged, preventing potential increases of 1–4% across most income ranges next year. The increased standard deductions from the TCJA are also now permanent. Additionally, the bill includes several notable changes: the lifetime gift and estate tax exemption has been permanently increased to $15 million; enhanced child credits have been raised; and the 20% qualified business income (QBI) deduction has been made permanent.

According to Strategas Research, cementing the TCJA tax provisions helped middle-class families avoid around a $400 billion tax increase in 2026.

Federal Deductions Temporarily Increased

The limit on federal deductions for state and local taxes (SALT) was temporarily raised from $10,000 to $40,000 ($20,000 for married couples filing separately) starting in 2025. The bill also included a 1% annual increase to the deduction amount until 2029, after which it reverts back to $10,000 in 2030. The deduction amount begins to decrease for incomes exceeding $500,000 ($250,000 for single filers).

The increase to the SALT deduction sparked controversy, as it not only added to the total cost of the bill but also because many believe it primarily benefits wealthy residents of high-tax states, such as New York and California. Residents of high-tax states, particularly upper-middle-class and high-income households who itemize deductions, will benefit most. According to the Tax Foundation, earners in the 95th to 99th income percentiles would see a 0.6% relative increase in after-tax income, while the bottom 80% of earners could see no benefit.

Clean Energy Programs Targeted

Clean energy-related programs received notable cuts. The bill accelerates the phase-out of energy tax credits introduced by the Inflation Reduction Act of 2022. This particularly affects solar and wind facilities, which now face shortened deadlines to qualify for credits. Specifically, projects must begin construction within 12 months of the bill's enactment to qualify for federal credits, while projects starting after this period must be in service by December 31, 2027. Furthermore, any projects owned by or using material assistance from Prohibited Foreign Entities (PFE) may lose credit eligibility. (PFEs include certain foreign governments, military companies, and entities with significant foreign ownership or influence.)

Other tax credits related to battery storage, hydro, geothermal, nuclear, carbon capture, and clean fuel remain in place.

For electric vehicles (EVs), the OBBBA eliminated the $7,500 Clean Vehicle Credit for new EVs and the $4,000 credit for used EVs for vehicles acquired after September 20, 2025. This is a notable change from the prior law, which allowed the credit for vehicles purchased through December 31, 2032.

New Deductions

The bill introduced new deductions for auto loan interest, overtime pay, tips, and Social Security payments.

Consumers who purchase a new car assembled in the United States can deduct up to $10,000 per year in interest paid on qualifying auto loans. The tax break incorporates purchases made between 2025 and 2028, and you won’t need to itemize to claim the deduction.

For Americans reliant on tips, eligible workers can deduct up to $25,000 in reported tip income from their federal income tax starting in 2025 (the deduction is phased out for incomes exceeding $150,000 and is set to expire in 2028). Workers can also deduct up to $12,500 in overtime pay, but similarly to tips, the deduction sunsets in 2028.

The bill also introduced a $6,000 tax deduction for seniors 65 or older who earn up to $75,000 a year (or $150,000 for couples) from 2025 to 2028. The deduction amount is lowered for incomes above that level and eventually phased out for higher incomes.

Increased Support for Businesses

New business expense and deduction provisions could boost growth and help offset headwinds from tariffs. Domestic research and development (R&D) costs can be 100% expensed in the year incurred or capitalized and amortized over five years (previous law). Qualifying capital equipment purchases can also be immediately expensed (100%) up until 2029. This allows companies to significantly reduce their tax burden in the year of the asset purchase and encourages businesses to invest in new property and equipment.

The bill also changes the way a company can claim interest expenses. The previous law allowed businesses to deduct interest expenses if they were less than 30% of earnings before interest and taxes (EBIT). However, the OBBBA now allows a business to deduct interest expenses up to 30% of earnings before interest, tax, depreciation, and amortization (EBITDA). Without getting into accounting, companies prefer the EBITDA approach because it simply means more interest expenses would be deductible (EBITDA is a larger figure than EBIT). This change could bode well for companies with higher debt burdens and/or higher amounts of depreciation and amortization expenses (small caps could be a notable beneficiary here).

Summary

There is a little bit of everything packed into President Trump’s OBBBA. Proponents tout its simplification of the tax code, the removal of uncertainty over the sunsetting TCJA tax provisions, pro-growth initiatives, an America-first framework, and its focus on protecting our borders and national security. Opponents believe it is too expensive, benefits the wealthy, threatens clean energy initiatives, and leaves too many Americans without healthcare or SNAP benefits. From an investor standpoint, healthcare insurers, especially with high Medicaid populations, the renewable energy space, and even longer-duration Treasuries could face headwinds from the bill, while small caps, defense and border security companies, and capital equipment and R&D intense firms could be outsized beneficiaries.

The bill does bring some certainty to the market regarding tax policy and the debt ceiling (the debt ceiling was raised by $5 trillion as part of the reconciliation bill), but it also raises questions about how economic growth and tariffs counterbalance its cost. While the White House has been flexible on tariff rates and timing, there have been limited trade deals and little clarity regarding where things stand with several of our major trading partners. Trump also announced that he would no longer extend or pause tariffs after August 1.

While the path to policy clarity may be bumpy, potential upside catalysts make us comfortable suggesting portfolio risk levels stay near benchmarks. Anticipate modest gains for stocks over the next six months with volatility in between.

Let's schedule a time to discuss how these changes affect your specific goals and see how we can optimize your plan accordingly.

For insights on how clients can take full advantage of the bill, check out LPL's Investor Guide below.

For How-to Video, click the link below. For How-to Tutorial with Images scroll to area below the video link.

Reach out to clients@plumtreefinancial.com with questions.

Watch PlumTree Financials' "Going Paperless" video tutorial for step-by-step instructions on how to turn on paperless settings in Account View. It is a quick and easy way to reduce client mailings, statements and tax forms.

How-to Tutorial with Images

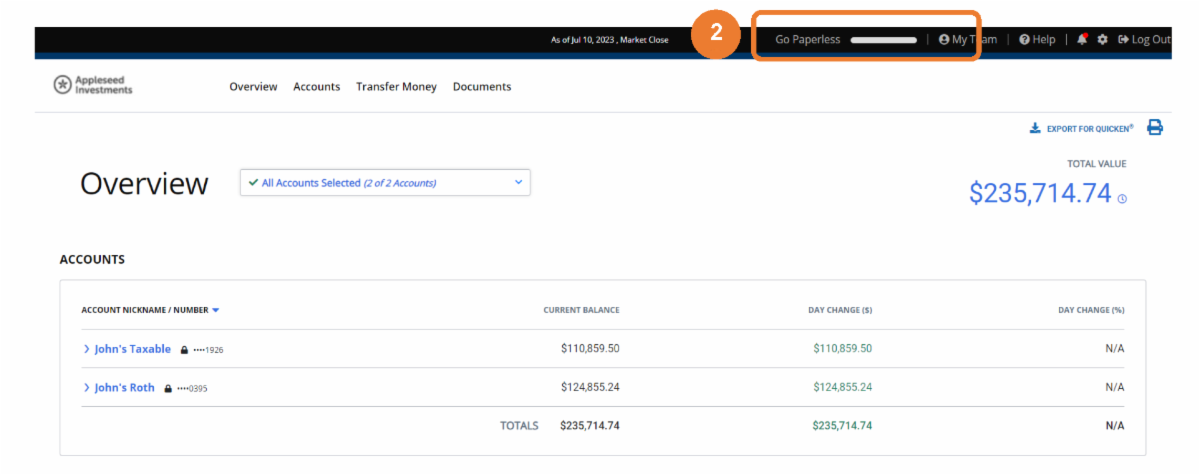

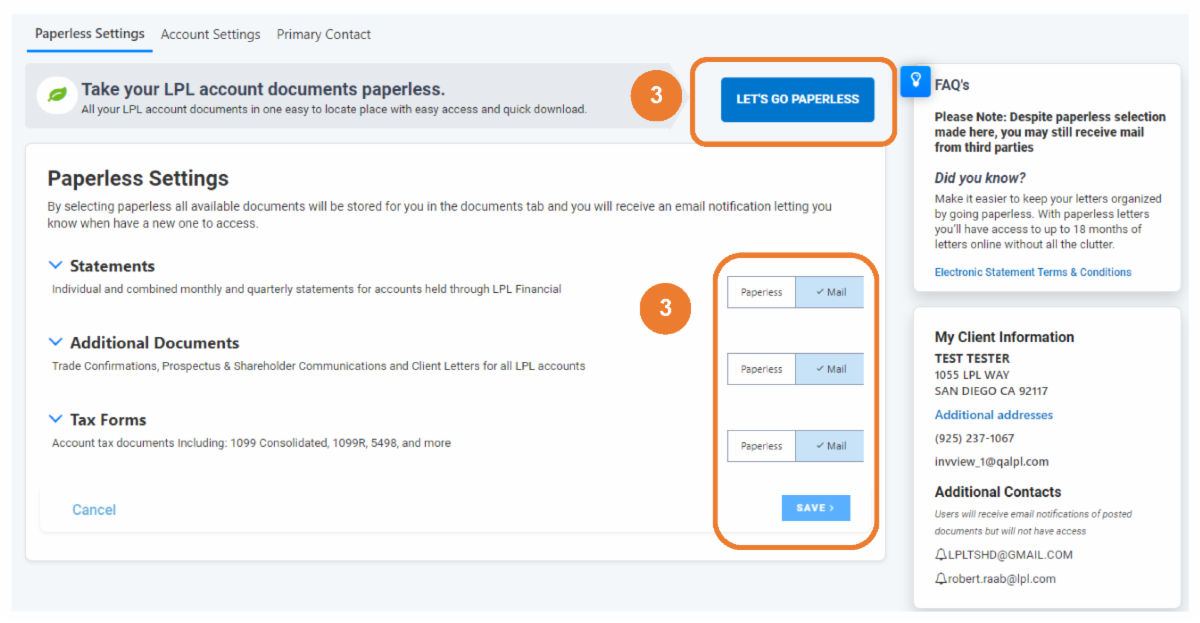

3 Steps to "Go Paperless"

1. Log in to your account at myaccountviewonline.com.

2.At the top of the page where it says “Go Paperless” click on it.

3.From there you can choose to either go 100% paperless for all eligible documents or pick and choose what you receive paperless and by mail delivery.

Hanging out with us in the Plum Tree!

Mid-Year Financial Tune-Up

It is hot outside—making now the perfect time to pause, reflect, and realign. A mid-year financial check-in helps you spot patterns, adjust course, and plan ahead with clarity. By reviewing your budget, savings, and goals now, you can make smart, intentional choices for the rest of the year—before the pace picks up.

Use the downloadable checklist to guide your tune-up and stay financially focused through December.

Have questions or need assistance customizing this resource to fit your goals? PlumTree Financial is here to support your financial clarity and growth—every step of the way.

Think You Know Every Racquet Sport? Discover Court Tennis

If you believe you are familiar with every racquet sport, court tennis may surprise you. Also known as real tennis, it is the original form of the game, with roots in 12th-century France. First played by monks and later embraced by European nobility—including England's King Henry VIII—court tennis is steeped in history.

Unlike modern tennis, court tennis is played indoors on a complex, asymmetrical court with sloping roofs called penthouses, odd angles, and openings built into the walls. Players use handmade cork-core balls and heavy wooden racquets with off-center heads, crafted specifically for the game's unique design and unpredictable bounces.

Today, fewer than 50 courts remain worldwide, but the sport continues to thrive among a dedicated community. Court tennis is not only a test of skill and strategy—it is a living connection to the origins of racquet sports.

Gregor Bernhard started playing tennis at an early age, but it was discovering Court Tennis a few years ago that truly ignited his passion. He has since traveled to several courts and become an active member of a young, vibrant community of players.

Have a unique sport or travel obsession? A blooming garden tip or a story that is itching to be told? We would love to shine a spotlight on you!

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third-party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #766061

Account View 2.0 - How-to Go Paperless Guide for Investors

This material was prepared by LPL Financial.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL Financial affiliate, please note LPL Financial makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency

Not Bank/Credit Union Guaranteed

Not Bank/Credit Union Deposits or Obligations

May Lose Value

Member FINRA/SIPC.

Tracking #1-05123778 (Exp. 3/2024)

Securities and Advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC. Insurance products offered through LPL Financial or its licensed affiliates.

All information is believed to be from reliable sources; however, PlumTree Financial makes no representation as to its completeness or accuracy.