This month’s issue brings a mix of timely insights and long‑term perspective as we head into summer. We break down market momentum in "Technical Take on the Record High Rally," help families prepare for the next big milestone in "Countdown to College," and continue empowering new investors with our Young Investor’s Series presentation, "Invest Now! Or Pay Later..." We are also keeping our 2026 goals spotlight rolling this month, featuring Robin’s thoughtful perspective and signature humor.

As a quick note: we will be pausing the newsletter for July and August to recharge and gather fresh insights. We will be back in September with more ideas, analysis, and stories to share.

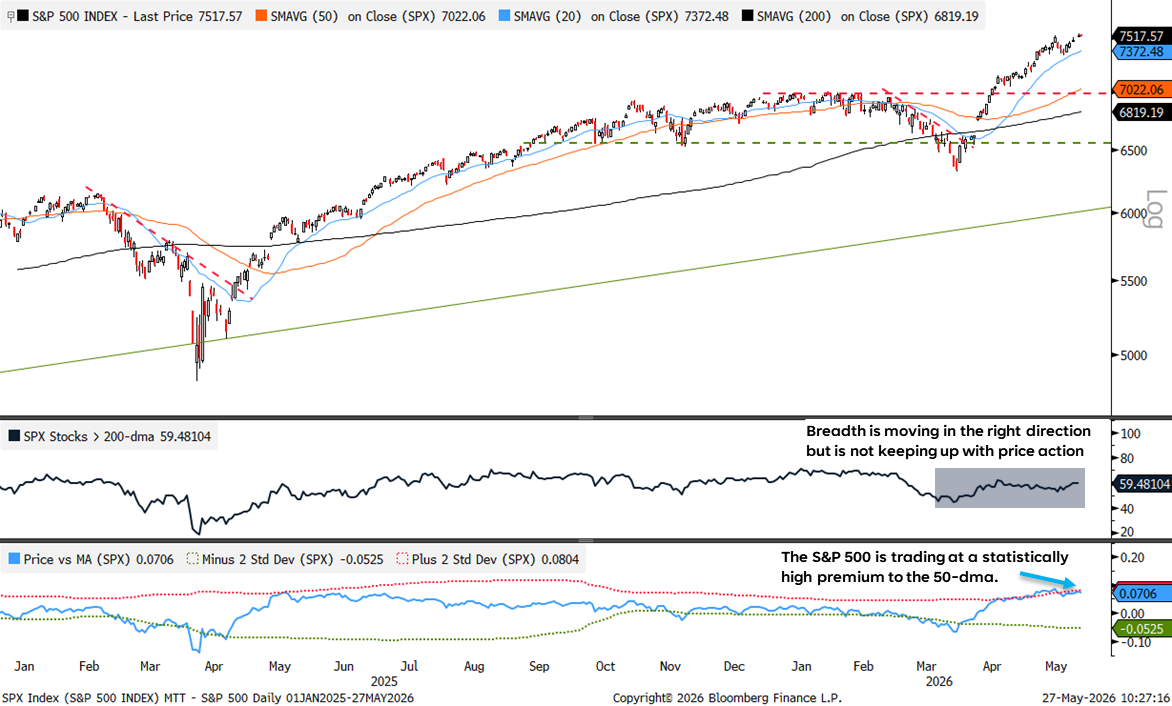

Risk appetite remains firmly intact as optimism surrounding a potential resolution to the war with Iran continues to improve investor sentiment. The S&P 500 has now advanced for eight consecutive weeks, with price action remaining remarkably resilient throughout the recovery. Since bottoming on March 30, the index has gained roughly 18% over just 39 trading sessions, producing an average daily gain of more than 0.8% while experiencing a maximum drawdown of only 1.2% during the advance. While easing geopolitical tensions and an ongoing ceasefire framework have provided a major catalyst for the rally, strong corporate earnings have also played a critical role in sustaining momentum.

According to LPL Chief Equity Strategist Jeffrey Buchbinder, first-quarter S&P 500 earnings growth is currently tracking near 28% year over year. The Magnificent Seven accounted for more than 15 percentage points of that growth, though the remaining “S&P 493” are still expected to deliver earnings growth near 20%, highlighting that underlying fundamentals outside of mega cap technology remain healthy.

From a technical perspective, the S&P 500 regained momentum quickly after gapping above its 200-day moving average (dma) in April and has since moved decisively to new record highs above the 7,000-point milestone. Momentum indicators continue to confirm the bullish trend, although several measures are now approaching short-term overbought territory following the magnitude and speed of the advance.

Market breadth, however, remains a more cautious part of the recovery story. Breadth indicators have diverged from price action over the last month, suggesting participation beneath the surface has not fully kept pace with the index-level rally. Currently, only about 60% of S&P 500 constituents are trading above their 200-dma, below the historical average of roughly 73% typically seen when the index is making new highs. Still, narrow breadth has not prevented this large cap-led bull market from extending higher, as periods of concentrated leadership have often been followed by broader sector and style rotations once mega cap momentum begins to cool.

A similar pattern unfolded last year when large cap technology stocks led the market sharply higher off the April lows before eventually consolidating as leadership broadened into value stocks, small caps, and other cyclical areas of the market last fall. The current environment appears to be following a comparable script, with mega cap technology and semiconductor-related names once again carrying much of the market through major resistance levels.

Technology leadership remains exceptionally strong, with the sector continuing to reach new highs on both an absolute and relative basis. However, increasingly stretched momentum conditions and elevated positioning suggest the rally may be becoming more vulnerable to short-term consolidation. Semiconductor and memory-related stocks have experienced parabolic advances since the March lows, with several momentum indicators reaching historically elevated levels. While overbought conditions alone are not necessarily bearish, the probability of near-term profit taking or rotational activity appears to be rising as investor positioning becomes increasingly crowded.

Records on Repeat for the Broader Market

Source: LPL Research, Bloomberg 05/27/26

Disclosures: Past performance is no guarantee of future results. All indexes are unmanaged and cannot be invested in directly.

Internal Outperformance

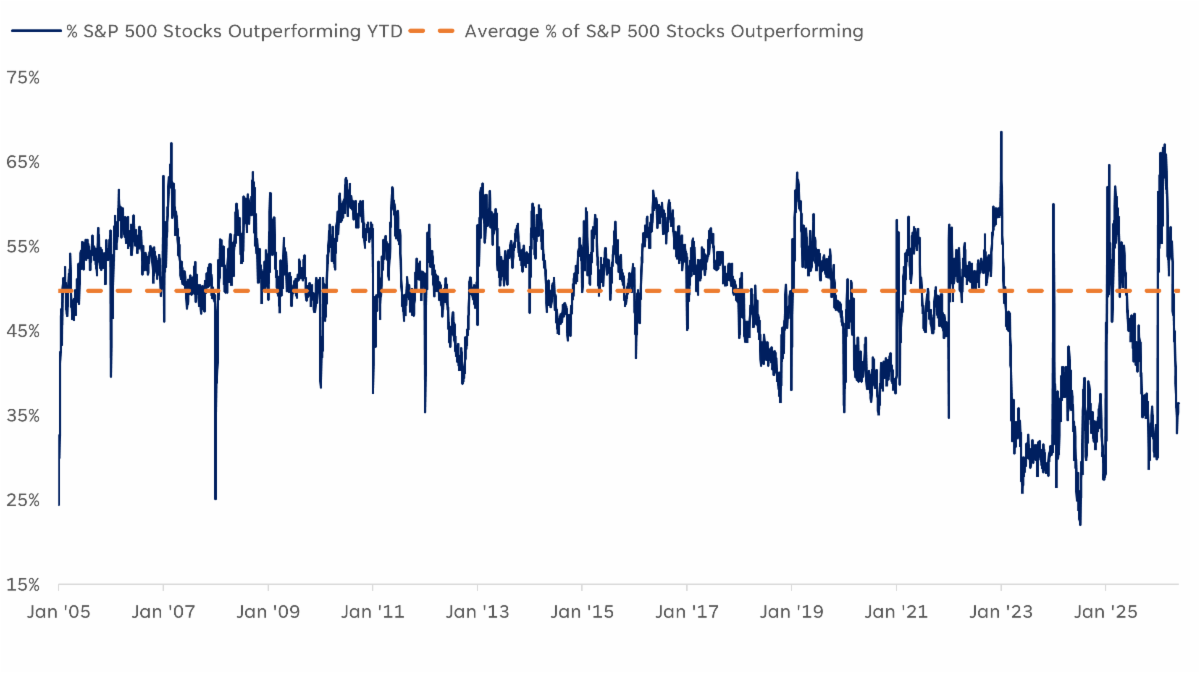

Another way to assess participation is to analyze how many stocks are outperforming the broader index. As the rotation from last fall gained traction into 2026, just over two-thirds of S&P 500 constituents were outperforming the index on the year in mid-February. Historically, that level has represented the upper end of participation breadth over the last two decades in our dataset.

Since then, leadership has rotated back toward growth and big tech, driving the percentage of stocks outperforming the index down to roughly 33% earlier this month. That level is approaching a historically narrow participation extreme, which has often preceded broader market rotations. In fact, following the previous seven instances where internal outperformance reached similarly depressed levels, large cap value and small cap stocks outperformed both large cap growth and the broader S&P 500 over the subsequent one-, three-, and six-month periods.

Historically Narrow Leadership May Be Setting the Stage for Rotation

Source: LPL Research, FactSet 05/26/26

Disclosures: Past performance is no guarantee of future results. All indexes are unmanaged and cannot be invested in directly.

Conclusion

The S&P 500 continues to exhibit strong momentum, supported by growing optimism surrounding a resolution to the conflict with Iran and the eventual reopening of the Strait of Hormuz. Corporate earnings have provided another important tailwind, particularly within large cap technology, where strong results continue to reinforce the longer-term artificial intelligence growth narrative. At the same time, increasingly stretched momentum conditions are beginning to emerge following the market’s largely one-way advance, especially across semiconductor and memory-related stocks that have experienced parabolic moves higher in recent months.

Investor sentiment and positioning within the technology space have also become increasingly crowded from a contrarian perspective, leaving us somewhat cautious over the near term as the probability of consolidation or a pullback appears elevated. Longer term, we remain constructive on the secular bull market backdrop but recognize market advances rarely unfold in such a linear fashion. In addition, historically low levels of internal outperformance continue to suggest the potential for a broader rotation away from concentrated large cap growth leadership and into other areas of the market.

Did You Know?

Countdown to College

As a parent, you of course want to give your child the best opportunity for success, and for many, attending the “right” university or college is that opportunity. Unfortunately, being accepted to the college of one’s choice may not be as easy as it once was. Additionally, the earlier you consider how you expect to pay for college costs, the better. Today, the average college graduate owes $38,375 in debt, while the average salary for a recent graduate is $68,516.1,2

Preparing for college means setting goals, staying focused, and tackling a few key milestones along the way—starting in the first year of high school.

Freshman Year

Before the school year begins, you and your child should have at least a handful of colleges picked out. A lot can change during high school, so remaining flexible but focused on your shared goals is crucial. It may be helpful to meet with your child’s guidance counselor or homeroom teacher for any advice they may have. You may want to encourage your child to choose challenging classes as they navigate high school. Many universities look for students who push themselves when it comes to learning. However, a balance between difficult coursework and excellent grades is important. Keeping an eye on grades should be a priority for you and your child as well.

Sophomore Year

During their sophomore year, some students may have the opportunity to take a practice SAT. Even though they won’t be required to take the actual SAT for roughly a year, a practice exam is a good way to get a feel for what the test entails.

Sophomore year is also a good time to explore extracurricular activities. Colleges are looking for the well-rounded student, so encouraging your child to explore their passions now may help their application later. Summer may also be a good time for sophomores to get a part-time job, secure an internship, or travel abroad to help bolster their experiences.

Junior Year

Your child’s junior year is all about standardized testing. Every October, third-year high-school students are able to take the Preliminary SAT (PSAT), also known as the National Merit Scholarship Qualifying Test (NMSQT). Even if they won’t need to take the SAT for college, taking the PSAT/NMSQT is required for many scholarships, such as the National Merit Scholarship.3

Top colleges look for applicants who are future leaders. Encourage your child to take a leadership role in an extracurricular activity. This doesn’t mean they have to be a drum major or captain of the football team. Leading may involve helping an organization with fundraising, marketing, or community outreach.

In the spring of their junior year, your child will want to take the SAT or ACT. An early test date may allow time for repeating tests during their senior year, if necessary. No matter how many times your child takes the test, most colleges will only look at the best score.

Senior Year

For many students, senior year is the most exciting time of high school. Seniors will finally begin to reap the benefits of their efforts during the last three years. Once you and your child have firmly decided on which schools to apply to, make sure you keep on top of deadlines. Applying early can increase your student’s chance of acceptance.

Now is also the time to apply for scholarships. Consulting your child’s guidance counselor can help you continue to identify scholarships within reach. Billions in free federal grant money go unclaimed each year, simply because students fail to fill out the free application. Make sure your child has submitted their FAFSA (Free Application for Federal Student Aid) to avoid missing out on any financial assistance available.4

Finally, talk to your child about living away from home. Help make sure they know how to manage money wisely and pay bills on time. You may also want to talk to them about the social pressures some college freshmen face for the first time when they move away from home.

For many people, college sets the stage for life. Making sure your children have options when it comes to choosing a university can help shape their future. Work with them today to make goals and develop habits that will help ensure their success.

Hanging out with us in the Plum Tree!

Young Investor's Series: Invest Now! Or Pay Later...

A Financial Planning Webinar for Young Investors

Purpose:

To help young investors begin a financial plan that initiates goal setting, budgeting, investing, and retirement planning.

Presenters:

Greg Bernhard, CFP® MBA

Brock Mumford, Client Service Associate, MBA

Date & Time:

August 19, 2026, 12PM EST

You do not need to have money to start planning for it.

Join Greg and Brock for Invest Now! Or Pay Later…, an informative webinar designed to help young adults begin building a strong financial foundation. Learn the basics of goal setting, budgeting, investing, and retirement planning, and discover how the financial decisions you make today can impact your future.

Many people wait to start planning because they think they do not have enough money. The truth is that time is your greatest asset. Starting early gives you the opportunity to develop smart financial habits, take advantage of long-term growth opportunities, and create a roadmap for achieving your financial goals.

Whether you are a student, recent graduate, or young professional, this webinar will provide practical tools and strategies to help you get started on your financial journey and make informed decisions about your future.

This webinar is the first in a series focused on financial empowerment and wealth building. Stay tuned for additional webinars and educational sessions as we continue to help participants build financial knowledge, confidence, and a strong foundation for long-term financial success.

We are continuing our journey into the Plums’ plans, ambitions, and delightfully offbeat perspectives for 2026. This month, we are spotlighting Robin, whose blend of humor and thoughtful perspective always stands out.

Upcoming Events

Save the Date

July 16, 2026 | 12pm EST

Save the Date - LPL Mid-Year Market Outlook

Get fresh insights, data, and perspective on how the markets are evolving — and what to expect in the months ahead.

We will be joined by Adam Turnquist, LPL Financial's Chief Technical Strategist.

Start the summer strong. Follow us for financial insights, market perspectives, and practical tips to help you make the most of every opportunity.

Blue-Chip Stocks - The term "blue chip" did not originate on Wall Street—it came from poker. In the game, blue-colored chips traditionally held the highest value, making them a natural symbol for quality and reliability. The expression was adopted by the financial world in the 1920s when market observers began using it to describe the stocks of large, well-established companies with strong reputations and consistent performance.

Over time, "blue-chip stock" became shorthand for companies known for financial stability, durable business models, and a history of weathering economic ups and downs. While blue-chip stocks are not immune to market volatility, they are often viewed as foundational holdings in long-term investment portfolios.

Today, the term remains widely used by investors seeking companies with proven track records, steady earnings, and the potential to deliver sustainable growth over time. Like the poker chips that inspired the name, blue-chip stocks are often associated with lasting value rather than speculation.

Citations

Countdown to College

1. EducationData.org, January 15, 2025

2. BankRate.com, May 17, 2024

3. PrincetonReview.com, 2025

4. EducationData.org, November 3, 2024

Diclosures

Technical Take on the Record-High Rally

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1115500

Countdown to College

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice.

It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.

This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm.

The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

Copyright FMG Suite.

Securities and Advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC. Insurance products offered through LPL Financial or its licensed affiliates.

All information is believed to be from reliable sources; however, PlumTree Financial makes no representation as to its completeness or accuracy.

The information contained in this e-mail message is being transmitted to and is intended for the use of only the individual(s) to whom it is addressed. If the reader of this message is not the intended recipient, you are hereby advised that any dissemination, distribution or copying of this message is strictly prohibited. If you have received this message in error, please immediately delete.