In this month’s newsletter, Greg chimes in with his own thoughts on the recently vacated DOL fiduciary rule and the low bar for 'fiduciaries' in the retirement planning business. We also explore why equities may continue to outperform the traditional “Sell in May” expectations, supported by strong market momentum, solid earnings, and favorable recent seasonality despite ongoing inflation and oil supply risks. Additionally, we introduce the PLUM strategy for financial housekeeping alongside a practical May money playbook focused on intentional spending, simple habit upgrades, and straightforward financial organization strategies to help align everyday choices with longer-term financial goals. Finally, to round out this issue, in the “Plum Picks” section, we feature another Plum's amusing reflections on 2026 goals.

The sharp rebound from the March lows has pushed most major equity indexes back to record highs. This upside momentum has been fueled in part by signs of de-escalation with Iran and growing expectations that the Strait of Hormuz could reopen soon. While the geopolitical environment remains fluid on a day-to-day basis, markets appear to be assigning a higher probability to a relatively near-term U.S. exit from the Middle East, alongside a normalization in global supply chains that could ultimately pressure oil prices lower.

Heading into month-end, the S&P 500 is up 9.2% as of April 29, putting it on pace for its strongest April performance since 2020. Support for equities has also come from solid first-quarter earnings and economic data that have shown limited signs of deterioration.

However, not all markets are sending the same signal. The physical oil market continues to reflect the risk of a “higher-for-longer” regime, suggesting tighter underlying supply conditions (a theme we explored further in Paper vs. Physical: What Tighter Oil Supplies Could Mean). The fixed income market also paints a similar story of lingering inflation risk as Treasury yields remain uncomfortably high. Although it's important to note, yields have been less responsive to higher oil prices this month versus last month.

May Seasonality: Weak History, Strong Recent Trends

As the calendar turns to May, seasonal trends re-enter the conversation. Historically, May has been a relatively lackluster month for equities. Since 1950, the S&P 500 has delivered an average return of just 0.4% and finished higher 62% of the time, ranking as the fifth-weakest month of the year when it comes to returns.

More recently, however, the data tells a different story. Since 2013, May has averaged a stronger 1.5% return, with 12 of the past 13 years ending in positive territory. This suggests that while long-term trends remain subdued, recent performance has been far more constructive.

Sell in May and Go Away?

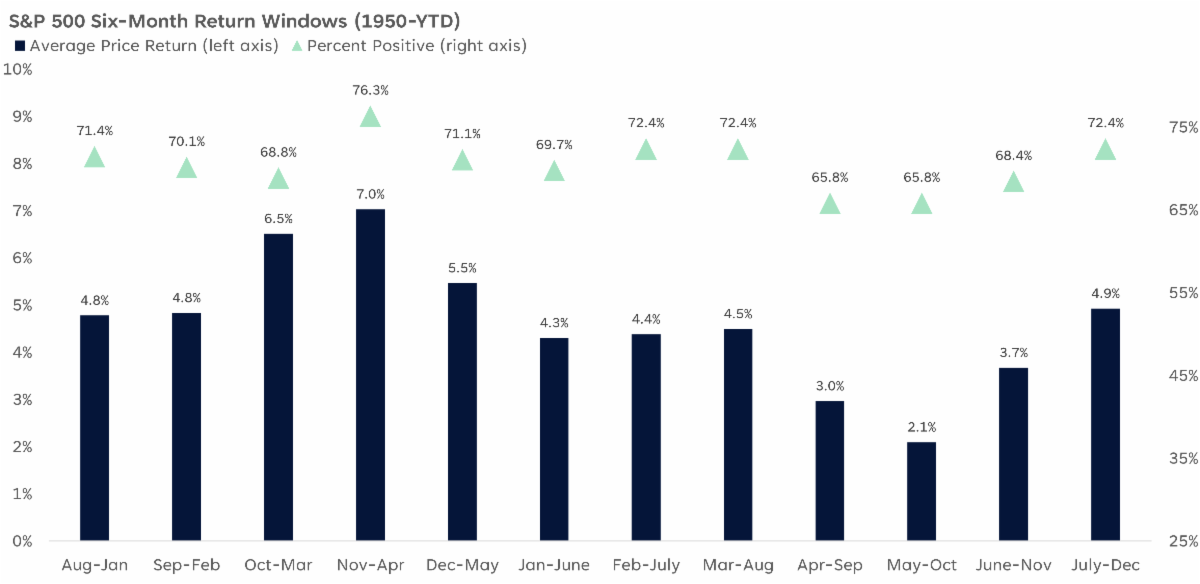

May also marks the beginning of the market’s traditionally weakest six-month period, lending support to the well-known “Sell in May and Go Away” adage. This phrase originated in London as “Sell in May and go away, come back on St. Leger’s Day,” referencing a historic horse race dating back to 1776. The idea suggests investors should step away from equities during the summer months and re-enter the market in November, when conditions have historically been more favorable.

The popularity of this saying likely stems from both its simplicity and the data behind it. Since 1950, the May–October period has produced the weakest six-month returns for the S&P 500, while November–April has been the strongest. Over time, this pattern, combined with the phrase’s widespread recognition, may have contributed to a degree of self-fulfilling behavior in markets.

Still, it’s important to keep this in perspective. While May through October has historically delivered a modest average gain of 2.1%, returns have been positive roughly two-thirds of the time over this period. More recently, performance has been even stronger. Over the past 12 years, median and average returns during this period were 6.3% and 5.1%, respectively, with positive outcomes in 82% of cases.

May–October Returns Tend To Be Underwhelming but Positive

Source: LPL Research, Bloomberg 04/29/26

Disclosures: Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly. The modern design of the S&P 500 stock index was first launched in 1957. Performance back to 1950 incorporates the performance of the predecessor index, the S&P 90.

Despite these seasonal trends, LPL Research does not advocate for investors to exit equities during this period. However, ongoing geopolitical uncertainty, particularly surrounding Iran, and its implications for growth and inflation are likely to keep volatility elevated. The reopening of the Strait of Hormuz, while potentially positive, introduces second-order effects that remain difficult to quantify at this stage.

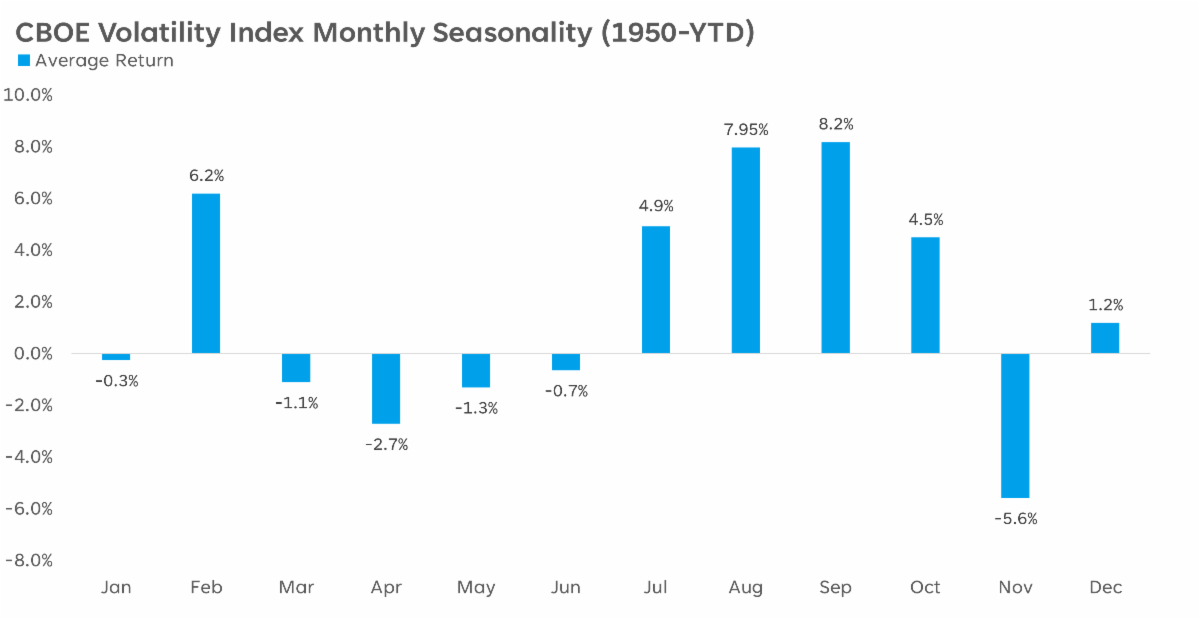

History also supports the expectation of increased volatility in the months ahead. The CBOE Volatility Index (VIX), often referred to as the market’s “fear gauge,” has historically trended higher from July through October, typically peaking in late September or early October. The VIX measures expected 30-day volatility based on S&P 500 options pricing; higher readings generally reflect increased uncertainty and risk aversion.

Volatility Tends To Ramp Up Into the Fall

Source: LPL Research, Bloomberg 04/29/26

Disclosures: Past performance is no guarantee of future results. All indexes are unmanaged and can’t be invested in directly.

Summary

Seasonal patterns can offer useful historical perspective, but they aren’t always a reliable guide for what lies ahead. Market direction will depend more on current forces, particularly geopolitical developments and oil prices, along with key fundamentals such as earnings, economic growth, inflation, the labor market, and monetary policy. An easing of tensions in the Middle East and a pullback in oil prices could provide ongoing support for equities, especially if earnings remain resilient.

Did You Know?

The Fiduciary Rule is Dead (Again): What It Means for Your Retirement

On March 12, 2026, a federal court in Texas officially vacated the 2024 Department of Labor (DOL) "Retirement Security Rule," effectively ending the most recent attempt to expand fiduciary protections for retirement investors. While this may be hailed as a "regulatory win" in some corners of the financial industry, the reality for investors—and particularly for retirees—is much more concerning.

The Protection Gap

The death of this rule means we are returning to the 1975 "five-part test" to determine who is a fiduciary. Under this old framework, many one-time financial moves—the most significant of which is the 401(k) rollover—are no longer automatically subject to a fiduciary standard.

For many retirees, the decision of what to do with a lifetime of savings at the point of retirement is the single most important financial choice they will ever make. Without a universal fiduciary requirement, individuals are once again vulnerable to "advice" that may be driven more by high commissions or proprietary product sales than by what is actually best for the client’s long-term security.

The Wrong Messenger

While the protection of investors is paramount, there is a valid argument that this specific rule was flawed from the start because of its origin. The Department of Labor attempted to stretch its authority under ERISA (the Employee Retirement Income Security Act of 1974) to regulate areas that the statute likely never intended to cover.

Public policy regarding financial advice should be clear and consistent, but it should ideally come from a legislative framework or a primary securities regulator rather than being shoehorned into labor laws. The "pendulum swing" of fiduciary rules—where protections are enacted by one administration and dismantled by the next via the courts—creates a landscape of "regulation by litigation" that leaves both advisors and clients in a state of constant uncertainty.

The "Low Bar" of the RIA Standard

Even within the world of Registered Investment Advisors (RIAs), the term "fiduciary" has become somewhat diluted. In our industry, the barrier to entry for becoming an RIA or a "fiduciary" advisor is surprisingly low. A firm can register, check the necessary boxes, and technically claim fiduciary status without necessarily possessing the deep technical expertise required to navigate complex tax, estate, and retirement strategies.

Being a fiduciary is a legal obligation, but it is not a guarantee of competence. Investors often assume that because an advisor is a fiduciary, they are operating at the highest level of professional skill. Unfortunately, the "RIA standard" alone does not always reflect the rigor that a client’s life savings deserves.

The Gold Standard: Why the CFP® Matters

This is why the CFP® (Certified Financial Planner) designation remains the gold standard. To earn and maintain the CFP® mark, an advisor must meet extensive education, examination, and experience requirements that go far beyond basic licensing. More importantly, the CFP Board's own Standards of Conduct require a CFP® professional to act as a fiduciary at all times when providing financial advice.

If a professional appears to the public to be providing financial advice, they should be held to a higher standard—period. Whether through the CFP® designation or a similarly rigorous set of professional requirements, the industry needs to move toward a model where "advice" is not a marketing term, but a professional service backed by a high bar of entry and an unwavering commitment to the client's best interest.

For now, as the regulatory landscape shifts back to the status quo, the burden of due diligence falls back onto the investor. It is more important than ever to look past the titles and ask your advisor: Are you a fiduciary in every interaction? And what specific credentials back up that promise?

Hanging out with us in the Plum Tree!

Hot Dogs, High Yields & Halfway There: Your May Money Playbook

May is not just about warmer weather and weekend plans. It is also the unofficial start of summer spending season. Translation: more invitations, more travel, more reasons to swipe your card. Instead of fighting it, let us make your money work with your lifestyle this month.

The “Fun Budget” Rule

Here is a twist: instead of trying to cut back on everything, decide in advance what you are excited to spend on this month. Concerts, cookouts, quick getaways are all great.

Now cap it. Guilt-free spending works best when it has boundaries.

Upgrade One Habit (Not Your Whole Life)

Trying to overhaul your entire financial routine rarely sticks. Instead, pick one upgrade:

Automate your savings.

Pay an extra chunk toward debt.

Finally open that investment account.

One small shift done consistently beats a dozen abandoned plans.

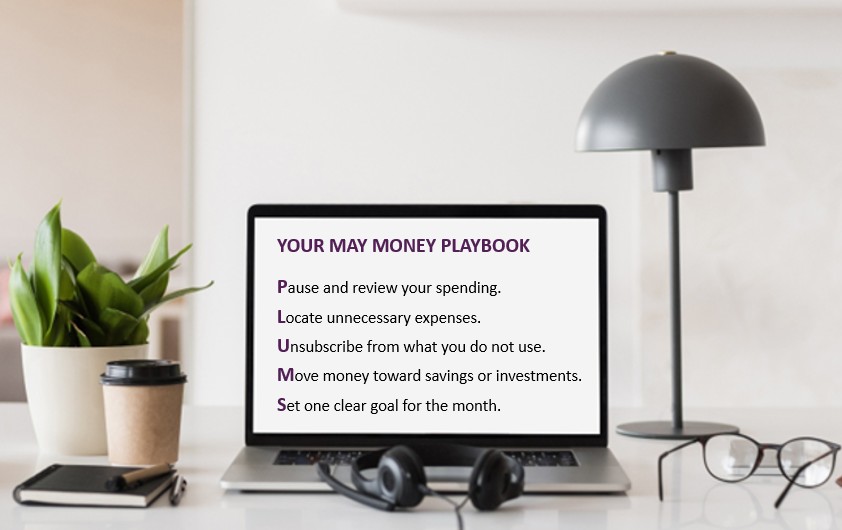

The PLUMS Strategy: Your Financial House Cleaning

The PLUMS have a spring-cleaning checklist for your financial house —simple, effective, and more satisfying than it sounds.

Pause and review your spending.

Locate unnecessary expenses.

Unsubscribe from what you do not use.

Move money toward savings or investments.

Set one clear goal for the month.

The Sneaky Cost of Convenience

May tends to bring “I will just…” spending:

“I will just grab takeout.”

“I will just take a ride.”

“I will just book it.”

Convenience is great, but it comes at a premium. This month, stay aware of when you are paying for ease versus value. A little intention here can save a lot without sacrificing fun.

Your Mid-Year Money Snapshot (No Stress Required)

You do not need a full financial overhaul, just a quick snapshot:

Are you saving something each month?

Is your debt going down?

Are you planning long term?

If you can answer yes to even one, you are building momentum.

The Bottom Line

You do not have to choose between enjoying life and being financially smart. The real win is designing a plan that lets you do both. If you need support along the way, our team is always here and ready to provide guidance whenever you need it.

Plum Picks: Where Petals Meet Passports

2026 Plans, Goals, and a Dash of Humor

We are back with another peek into the Plums’ plans, ambitions, and wonderfully quirky thoughts for 2026. This month’s feature highlights one of our favorite Administrative Associates, Kathy, bringing her signature blend of wit and wisdom. Check in next month to find out which Plum takes center stage.

Upcoming Events

Save the Date

May 28, 2026 | 1:30pm EST

Ask Sabrina!

Ask Sabrina is our Q&A session focused on navigating your accounts, accessing statements, and making the most of your tools.

No reservations are needed. Just join the meeting on the designated day and time by clicking the link provided.

Sabrina, Vice President of Client Services, looks forward to seeing you and answering your questions!

Young Investors Series: Invest Now! Or Pay Later...

Join Greg Bernhard and Brock Mumford (members of PlumTree Financial’s investment team) for an engaging session designed specifically for young investors ready to take control of their financial journey.

This webinar will guide you through the essentials of creating a financial plan, including setting meaningful goals, building a budget, starting to invest, and planning for retirement.

Make May the month you stay informed, stay ahead, and follow us for insights that keep your finances moving in the right direction.

In for a penny, in for a pound - The phrase originates from England’s old currency system, where a penny was a minimal amount and a pound a substantial sum, highlighting the dramatic difference between small and large financial stakes. It emerged in the late 17th century, with one of the earliest recorded uses appearing in a 1695 play by Edward Ravenscroft, showing it was already common speech at the time. Early meanings were tied to debt and punishment—suggesting that owing a penny could carry consequences similar to owing a pound, so one might as well risk the larger sum.

The explanation is tied to this idea of escalating commitment: once any amount—however small—has been risked, the logic (or temptation) is to go all in. The old, vivid idiom meaning that once you have begun investing money, effort, or reputation, you should fully commit—though in financial or business use, it often carries a cautionary undertone about doubling down on a risky or losing position rather than cutting losses

Disclosures

Sell in May and Go Away? Maybe Not

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk.

Indexes are unmanaged and cannot be invested into directly. Index performance is not indicative of the performance of any investment and does not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

This material was prepared by LPL Financial, LLC. All information is believed to be from reliable sources; however LPL Financial makes no representation as to its completeness or accuracy.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

Asset Class Disclosures –

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Bonds are subject to market and interest rate risk if sold prior to maturity.

Municipal bonds are subject and market and interest rate risk and potentially capital gains tax if sold prior to maturity. Interest income may be subject to the alternative minimum tax. Municipal bonds are federally tax-free but other state and local taxes may apply.

Preferred stock dividends are paid at the discretion of the issuing company. Preferred stocks are subject to interest rate and credit risk. They may be subject to a call features.

Alternative investments may not be suitable for all investors and involve special risks such as leveraging the investment, potential adverse market forces, regulatory changes and potentially illiquidity. The strategies employed in the management of alternative investments may accelerate the velocity of potential losses.

Mortgage backed securities are subject to credit, default, prepayment, extension, market and interest rate risk.

High yield/junk bonds (grade BB or below) are below investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.

Precious metal investing involves greater fluctuation and potential for losses.

The fast price swings of commodities will result in significant volatility in an investor's holdings.

This research material has been prepared by LPL Financial LLC.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Deposits or Obligations | Not Bank/Credit Union Guaranteed | May Lose Value

For Public Use – Tracking: #1100416

Securities and Advisory services offered through LPL Financial, a Registered Investment Advisor, Member FINRA/SIPC. Insurance products offered through LPL Financial or its licensed affiliates.

All information is believed to be from reliable sources; however, PlumTree Financial makes no representation as to its completeness or accuracy.